Impact of US-China Agreements on India GCC Business:

A white-paper for international-relations and business strategy decision makers. Prepared in the context of the May 2026 Trump-Xi state visit and related trade commitments

This white-paper assesses whether the recent US-China stabilisation package changes the strategic rationale for China+1 and, by extension, whether it alters the growth trajectory of Global Capability Centers (GCCs) in India. The analysis distinguishes between confirmed commitments, preliminary/institutional mechanisms, and forward-looking implications. It deliberately avoids treating every political announcement as a binding treaty or as an immediate change in corporate operating models.

Core conclusion: the agreements reduce near-term trade-war volatility and may soften the fear-driven China+1 narrative in selected sectors. However, they do not reverse India’s GCC opportunity because India’s GCC growth is now anchored as much in talent, AI, product engineering, cybersecurity, data, cost-to-capability arbitrage and global operating resilience as in China+1 supply-chain risk.

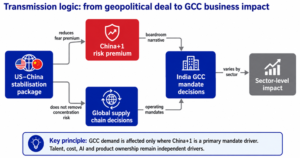

Figure 1. How US-China stabilisation transmits into GCC business decisions.

Executive Summary:

The May 2026 Trump-Xi visit produced a stabilisation package rather than a comprehensive strategic reset. Confirmed elements include two bilateral economic institutions, agricultural purchase commitments, aircraft-related arrangements, beef and poultry market access, and Chinese undertakings to address U.S. concerns over rare earths and critical minerals. A Chinese government source describes the framework as expanding two-way trade under a reciprocal tariff-reduction approach and establishing trade and investment councils, while the White House describes these as Boards of Trade and Investment. [S1, S2]

From a macroeconomic point of view, the package can reduce volatility in selected goods markets, redirect part of China’s commodity imports toward the United States, lower short-term risk around selected non-sensitive goods, and create a negotiation channel for tariffs and investment frictions. It does not eliminate strategic rivalry, export-control risk, industrial-policy competition, Taiwan/South China Sea risk, supply-chain concentration risk, or the incentive for companies to preserve optionality outside China.

For India GCCs, the net impact is selective and moderate, not disruptive. The strongest impact will be seen in sectors where GCC mandates are tied to manufacturing network redesign, electronics, semiconductors, automotive/EV, industrial engineering, and critical-input supply chains. The lowest direct impact will be seen in enterprise technology, AI/data, cybersecurity, BFSI, healthcare/pharma analytics, and corporate shared services, where the India rationale is dominated by skilled talent, product ownership, cost-to-capability, global process ownership and innovation mandates.

The strategic message for India GCC advisors should therefore shift from “China+1 because China is risky” to “India as a resilient enterprise nerve centre.” This is consistent with current GCC evidence: Nasscom-Zinnov data reported in 2026 indicates India hosts 2,117 GCCs across 3,728 units, employs approximately 2.36 million professionals, has ecosystem revenue of US$98.4 billion, and has more than 1,200 GCCs embedding AI/ML capabilities. [S6]

|

Question |

Assessment |

Evidence base |

| Do the agreements reverse China+1? | No. They may reduce urgency in specific goods categories, but China+1 is a broader de-risking strategy, not a tariff-only decision. | White House; China State Council/Xinhua; ISIS Malaysia research note. |

| Do they weaken India GCC growth? | Not materially. They may change narrative and timing for selected manufacturing-linked GCCs, while AI/product/cyber/BFSI mandates remain resilient. | Nasscom-Zinnov; Reuters; EY GCC Pulse. |

| Which sectors are most exposed? | Semiconductor/electronics design, automotive/EV, aerospace/aviation and supply-chain/procurement GCCs. | Deal includes critical minerals, aircraft, agriculture and tariff/non-tariff mechanisms. |

| What should India GCC sellers do? | Move from geopolitical pitch to capability, governance, AI-native operating model and enterprise resilience pitch. | GCC maturity shift and EY findings on AI, shared decision ownership and innovation teams. |

Figure 2. Confirmed deal/commitment stack based on public reporting and official releases.

What was agreed – Fact base and Evidence status:

The public record should be read carefully. Some components are clearly documented by official U.S. and Chinese sources; some are commercial commitments attributed to the summit; and some remain framework-level rather than legally detailed treaty text. The analysis below therefore classifies each item by evidence status.

|

Agreement / commitment |

Evidence status | What it means |

Macro trade implication |

| U.S.-China Board of Trade / Trade Council | Officially confirmed | A government-to-government forum to manage bilateral trade across non-sensitive goods and discuss tariff reductions/product issues. | Lowers transaction uncertainty; creates a channel for dispute management but does not guarantee tariff elimination. |

| U.S.-China Board of Investment / Investment Council | Officially confirmed | A forum for investment-related issues. | Could support selective cross-border investment flows; existing national-security screening is expected to remain relevant. |

| Reciprocal tariff-reduction framework | Confirmed at framework level | China’s state media/government portal says teams will expand two-way trade under a reciprocal tariff-reduction framework. | Reduces escalation risk in selected goods; may reduce China+1 urgency where tariffs were the dominant driver. |

| Rare earths and critical minerals | Officially referenced by White House | China will address U.S. concerns around shortages and restrictions on rare earths and critical minerals including yttrium, scandium, neodymium and indium. | Very relevant to electronics, EV, defense, clean energy and semiconductor supply chains; details and enforceability remain critical. |

| Boeing aircraft purchase | Officially referenced by White House; also reported by SCMP | China approved an initial purchase of 200 Boeing aircraft. SCMP also reported arrangements around engines and components. | Positive for U.S. aerospace manufacturing; limited direct effect on Indian GCCs except aviation engineering/digital operations mandates. |

| Agricultural purchases | Officially referenced by White House and Reuters | At least US$17bn per year of U.S. agricultural purchases in 2026-2028, in addition to earlier soybean commitments. | Can redirect Chinese demand from Brazil, Australia, Canada and others; macro impact is commodity-specific, not a broad manufacturing reset. |

| Beef market access | Officially referenced by White House and Reuters | China restored/renewed listings for over 400 U.S. beef facilities and added new listings; Reuters reports 425 extensions and 77 new approvals. | Trade access improvement; limited direct GCC impact. |

| Poultry imports | Officially referenced by White House | China resumed poultry imports from U.S. states determined by USDA to be free of highly pathogenic avian influenza. | Limited direct GCC impact; strengthens agricultural-trade thaw narrative. |

| Prior soybean, rare earth and tariff truce layer | Officially referenced in Nov 2025 White House fact sheet | China committed to 25 MMT/year of soybeans in 2026-2028; suspension/removal of certain retaliatory tariffs and non-tariff measures; U.S. extended some tariff suspensions. | Forms the baseline from which May 2026 agreements deepen stabilisation. |

Important caveat: these are not the same as a full free-trade agreement or a comprehensive bilateral treaty. The credible interpretation is a “managed rivalry” framework: both countries are reducing immediate economic friction where commercially useful while preserving strategic competition in technology, national security, data, industrial policy and regional geopolitics.

Macroeconomic implications for Global Trade:

The agreements matter because the United States and China remain anchor economies in global trade. However, the sectoral composition of the deal is important. The most concrete commitments are in agriculture, aircraft and critical inputs. These affect trade flows, commodity sourcing and supplier bargaining power, but they do not automatically rebuild the pre-trade-war globalisation model.

Immediate macro effects

- Lower volatility premium in selected goods. The Board/Council mechanism creates an escalation-management channel, which can reduce the probability of abrupt tariff shocks in covered non-sensitive goods. [S1, S2]

- Commodity trade diversion. Reuters analysis indicates that China’s US$17bn annual farm purchase pledge, in addition to soybeans, could lift U.S. farm exports to China toward US$28-30bn annually, below the 2022 peak but far above 2025 levels. This is likely to redirect purchases away from Brazil, Australia, Canada and other suppliers in some commodities. [S3]

- Targeted supply-chain relief, not complete de-risking reversal. Rare earth and critical mineral assurances could reduce immediate bottleneck risk for U.S. and global manufacturers, but details around licensing, compliance and future export controls remain decisive. [S1, S4]

- Business confidence effect. The mere existence of trade and investment councils lowers uncertainty for firms with existing China exposure, but a council is a process mechanism, not a guarantee of durable political alignment.

- Strategic rivalry remains. The agreements do not remove export-control competition, data-localisation risk, cyber concerns, Taiwan/South China Sea risk, or industrial subsidy competition.

The likely macro outcome is not “globalisation returns” but “fragmentation becomes more managed.” This distinction matters for GCC strategy because the India GCC case does not rest only on tariff avoidance. It rests on enterprise capability, talent depth, technology capacity, risk distribution and global process ownership.

Impact on global China+1 policy:

China+1 is best understood as a de-risking strategy in which companies maintain a China presence while adding alternative manufacturing, sourcing, technology or operating hubs elsewhere. The ISIS Malaysia research note describes China+1 as corporate diversification beyond China to mitigate dependence on China’s market or supply chain, while noting that China’s integrated manufacturing ecosystem cannot be easily replicated and that shifts are gradual. [S8]

The May 2026 agreements change one driver of China+1—tariff escalation risk—but do not remove the other drivers: overdependence, geopolitics, regulatory unpredictability, pandemic-learned resilience, labour-cost shifts, critical-mineral concentration, customer-market proximity and board-level operational continuity.

|

China+1 driver |

Effect of US-China agreements |

Residual risk / continued reason for China+1 |

| Tariff escalation | Partly reduced for selected goods through reciprocal tariff framework and councils. | Durability uncertain; product scope and future political cycles remain relevant. |

| Non-tariff barriers | Partly reduced for selected agricultural categories. | Manufacturing, technology, data and security barriers remain outside full resolution. |

| Critical minerals / rare earths | Potentially reduced if commitments are implemented reliably. | Supply still concentrated; firms may continue redundancy planning. |

| Technology rivalry | Mostly unchanged. | Export controls, AI chips, semiconductor equipment and IP/security issues remain strategic. |

| Operational concentration | Unchanged. | Boards still prefer multi-location resilience after Covid-era disruption and geopolitical shocks. |

| Cost and talent arbitrage | Unchanged. | China+1 locations can still offer cost, talent or market-access advantages. |

| Customer/regulatory proximity | Unchanged. | Regionalisation of operations remains a strong trend. |

Conclusion for China+1: the agreements may slow the most reactive form of China+1 in sectors where tariffs were the single dominant trigger. They do not reverse strategic de-risking in sectors where resilience, IP risk, customer proximity, national-security policy or supply-chain concentration are key drivers.

India GCC baseline before the agreements:

India’s GCC story has moved beyond labour arbitrage. Public 2026 reporting on Nasscom-Zinnov data states that India hosts 2,117 GCCs across 3,728 units, employs around 2.36 million professionals, has grown the number of GCCs by 32% since FY2021, includes 506 Forbes Global 2000 companies, and has a total ecosystem revenue of US$98.4bn. The same report highlights more than 1,200 GCCs with embedded AI/ML capabilities, over 250 dedicated Centers of Excellence, and roughly 250,000 AI professionals. [S6]

Reuters reported on 18 May 2026 that India is home to more than half of the world’s global centres, with companies attracted by skilled workforce, lower operating cost and ability to support high-value jobs across technology, finance and engineering. The same report also notes a more cautious hiring approach as companies adjust to geopolitical uncertainties and AI-led productivity, with some large-centre hiring plans being reduced by 30-50%. [S5]

EY’s 2025 GCC Pulse Survey reinforces the shift from cost centres to strategic hubs: 58% of India-based GCCs were investing in agentic AI, 83% in GenAI, 67% were creating dedicated innovation teams, and more than half held shared accountability for global decisions. [S7]

|

India GCC demand driver |

Relevance after US-China stabilisation |

Assessment |

| Digital and AI transformation | Very high | Unaffected or strengthened. Enterprises still need AI, data, platform and automation capabilities. |

| Global product engineering | Very high | Unaffected. India’s role is capability-driven, not tariff-driven. |

| Cost-to-capability arbitrage | High | Unaffected. Global cost pressures remain, and India remains a scale talent market. |

| Resilience / multi-location operating model | High | Partially affected. Fear premium softens, but continuity planning remains. |

| Manufacturing supply-chain redesign support | Medium to high | Potentially moderated in sectors where China stabilisation reduces urgency. |

| Innovation and decision ownership | High | Unaffected. EY data suggests India GCCs increasingly share or own global decisions. |

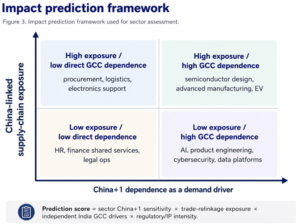

Prediction model and analytical framework:

Figure 3. Impact prediction framework used for sector assessment.

The prediction model uses a sector exposure matrix rather than a single macro conclusion. Each sector is scored through four lenses:

- China+1 dependence as a demand driver: whether GCC activity is triggered by supply-chain diversification rather than by ordinary digital transformation or cost-to-capability needs.

- Trade-relinkage exposure: whether the US-China agreements directly improve the sector’s trade economics, input availability or China-market access.

- Independent India GCC drivers: depth of India talent, AI/product/cyber capabilities, cost, existing GCC density and leadership maturity.

- Regulatory/IP intensity: whether national-security, export-control, data, IP or compliance risk remains high even after trade stabilisation.

This framework borrows from PESTLE for macro-environmental drivers, scenario planning for uncertainty, and exposure-based risk scoring for sector-level prediction. The prediction is not a deterministic forecast; it is an evidence-based directional view using public commitments and current GCC data.

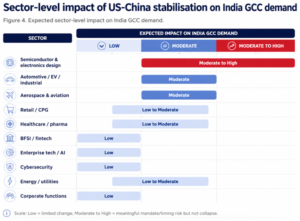

Sector-wise impact on India GCC business:

Figure 4. Expected sector-level impact on India GCC demand.

|

GCC sector |

Expected impact | Reasoning |

Strategic implication for India GCC business |

| Semiconductor & electronics design | Moderate to High | Critical minerals/rare earth relief and lower tech-supply friction may reduce emergency diversification pressure. However, technology rivalry, export controls and IP/security concerns remain. India design GCCs continue to benefit from VLSI, embedded, firmware, validation and AI-edge capabilities. | Position India as design, verification, embedded software and AI-edge hub rather than as a China substitute. |

| Automotive, EV and industrial engineering | Moderate | Rare earths, battery inputs and manufacturing networks are China-linked. Stabilisation can lower short-term supply anxiety, but OEMs still need multi-location engineering and software-defined vehicle capabilities. | Lead with software-defined vehicles, digital twins, embedded systems, PLM, supply-chain analytics and cost-to-capability. |

| Aerospace and aviation | Moderate | Boeing aircraft purchase strengthens US-China commercial aerospace ties, but it may also increase global engineering, aftermarket, MRO analytics and supply-chain digital work. | Pitch India GCCs for engineering services, digital operations, reliability analytics and supply-chain programme management. |

| Retail and CPG | Low to Moderate | Agriculture and commodity trade may affect sourcing and margins, but GCC demand is more connected to digital commerce, pricing, planning, customer analytics and supply-chain optimisation. | Focus on omnichannel platforms, AI merchandising, demand forecasting and global business services. |

| Healthcare, pharma and life sciences | Low to Moderate | Direct trade package impact is limited. China supply-chain considerations remain for APIs, devices and med-tech inputs; GCCs remain driven by R&D analytics, regulatory, pharmacovigilance and digital health. | Pitch regulatory analytics, clinical data platforms, AI-enabled R&D and global process ownership. |

| BFSI, fintech and insurance | Low | Minimal direct connection to goods trade. GCC mandates are driven by technology, risk analytics, cybersecurity, compliance operations, cloud and data. | Continue enterprise-tech and risk-transformation narrative. |

| Enterprise technology, software, AI and data platforms | Low | India’s advantage is talent and global product/platform ownership. US-China goods stabilisation does not reduce enterprise need for AI-native operating models. | Position as strategic engineering and AI governance centre. |

| Cybersecurity | Low | US-China stabilisation does not eliminate cyber, data and trust risks. If anything, strategic competition keeps security investment relevant. | Pitch security operations, product security, IAM, compliance automation and cyber AI. |

| Energy, utilities and clean-tech | Low to Moderate | Critical minerals and equipment supply chains can benefit from relief, but clean-tech supply chains remain strategically sensitive. | Build GCC cases around grid digitalisation, asset analytics, energy trading platforms and sustainability data. |

| Corporate functions: finance, HR, legal, procurement | Low | Trade agreements do not materially change the India business-services rationale. Procurement analytics may see some commodity-flow changes. | Pitch global process ownership, automation, compliance and shared-services optimisation. |

What changes for India GCC strategy:

The India GCC market is unlikely to lose momentum, but the sales narrative and operating model should evolve. A pure “China+1 flight from risk” pitch becomes less compelling if US-China trade channels remain stable. A stronger pitch is that India offers an enterprise transformation platform: AI-native talent, product engineering, cybersecurity, data, regulatory operations, and the ability to own global decisions.

|

Strategic shift |

Old narrative |

New recommended narrative |

| From fear to value | Move work to India because China is risky. | Build in India because India can own enterprise value creation, AI and global process outcomes. |

| From headcount to capability | Scale a large GCC quickly. | Build a smaller, AI-native core with flexible talent pools and measurable productivity. |

| From cost to cost-to-capability | India is cheaper. | India delivers superior capability per dollar in product, data, cyber and operational transformation. |

| From back office to nerve centre | India executes global work packages. | India co-owns decisions, standards, platforms and innovation roadmaps. |

| From single-location arbitrage to resilience | Replace China with India. | Maintain China where commercially necessary while adding India for digital, decision and operating resilience. |

This shift also aligns with current hiring signals. Reuters reported a more measured hiring approach in India GCCs because of geopolitical uncertainty and AI-led work redesign. Therefore, GCC advisory should emphasize operating-model quality, leadership architecture, governance, AI productivity, role design and outcomes rather than only seat-count growth. [S5]

Recommended GCC playbook by sector:

|

Sector |

Likely commercial implication |

Recommended India GCC service proposition |

| Technology / AI / SaaS | No meaningful reduction in GCC case. | Product/platform ownership, AI CoEs, responsible AI governance, cloud modernisation. |

| Cybersecurity | No reduction; strategic competition sustains security spending. | SOC modernisation, product security, threat intelligence, compliance automation. |

| Semiconductors/electronics | Narrative needs nuance; supply-chain relief may reduce urgency but not tech rivalry. | Chip design, embedded software, verification, firmware, EDA automation, IP security. |

| Automotive/EV | Moderated but resilient. | Software-defined vehicle platforms, battery analytics, embedded systems, PLM and sourcing analytics. |

| BFSI | Mostly unaffected. | Risk tech, regulatory operations, fraud analytics, cloud/data platforms. |

| Retail/CPG | Commodity impact possible, but GCC demand remains digital. | Merchandising AI, pricing, demand forecasting, customer ops and supply-chain control towers. |

| Healthcare/pharma | Limited direct impact. | Regulatory submissions, clinical analytics, pharmacovigilance, R&D data platforms. |

| Aerospace | Moderate opportunity from increased global activity. | Engineering analytics, MRO intelligence, manufacturing quality, supply-chain programme controls. |

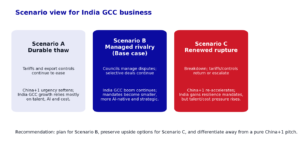

Scenario outlook:

Because trade agreements between strategic rivals are politically fragile, a scenario view is more appropriate than a single-point forecast. The base case is managed rivalry: selective trade normalisation alongside continued technology competition and de-risking.

Figure 5. Scenario outlook and implications for India GCC business.

|

Scenario |

Probability view | India GCC impact |

Recommended action |

| A. Durable thaw | Lower probability until there is evidence of sustained tariff and export-control rollback. | China+1 urgency reduces in manufacturing-linked sectors; India GCC growth continues on capability basis. | De-emphasize China risk; lead with capability, AI, cost-to-capability and global decision ownership. |

| B. Managed rivalry (base case) | Most plausible from current evidence: process mechanisms reduce volatility while rivalry remains. | GCC growth continues but becomes more selective, AI-native and productivity-led. | Build modular GCCs, flexible workforce models and sector-specific CoEs. |

| C. Renewed rupture | Plausible downside if enforcement fails or geopolitics worsen. | China+1 accelerates again; India gains mandates but talent/cost pressure and delivery risk rise. | Prepare rapid setup playbooks, location strategy, leadership hiring and transition governance. |

Implications for GCC advisory positioning:

For an India GCC advisory business, the strongest go-to-market response is to avoid over-indexing on “China+1” as the only trigger. Instead, build a composite proposition across five decision pillars: resilience, capability, AI, governance and speed-to-scale.

- Resilience: India as part of a multi-country operating model, not a simplistic China replacement.

- Capability: product engineering, data, AI, cybersecurity, process excellence and global business services.

- AI-native operating design: smaller core teams, productivity metrics, automation-first workflows and role redesign.

- Governance: decision rights, compliance, risk controls, information security, IP protection and enterprise-wide standards.

- Speed-to-scale: location strategy, legal entity setup, leadership hiring, transition governance, workspace, technology stack and operating cadence.

A practical sales message can be: “US-China stabilisation may reduce immediate tariff fear, but it does not remove the need for resilient, AI-native global operating capability. India GCCs are now enterprise nerve centres, not just China+1 overflow capacity.”

Risks, Caveats and Watch Indicators:

The analysis should be updated as implementation details become public. The most important watch indicators are:

|

Watch indicator |

Why it matters for China+1 |

Why it matters for India GCCs |

| Detailed tariff schedules under the Board/Trade Council | Determines whether stabilisation is broad or product-specific. | Manufacturing-linked GCC demand changes only if tariff relief is broad and durable. |

| Rare earth export licensing and actual shipment data | Tests whether critical-input risk is truly reduced. | Semiconductor, EV, electronics and clean-tech GCC mandates remain sensitive. |

| Export-control developments in AI chips, EDA tools and semiconductor equipment | Core technology rivalry may persist despite goods trade thaw. | India chip design, AI and cyber GCCs benefit from continued strategic segmentation. |

| Chinese agricultural import volumes by origin | Shows whether trade diversion from Brazil/Australia/Canada is material. | Limited direct GCC impact, but useful macro signal of deal compliance. |

| Boeing order execution and engine/component supply | Confirms aerospace commercial cooperation. | May create ancillary engineering, MRO and digital operations opportunities. |

| India GCC hiring and mandate mix | Indicates whether firms are cautious or expanding. | Signals demand for smaller AI-native GCCs versus large headcount-led centres. |

Conclusion:

The recent US-China agreements are meaningful because they reduce immediate trade-war volatility and create institutional channels for managing selected trade and investment issues. They are especially relevant to agriculture, aerospace, selected tariffs, non-tariff barriers and critical minerals. However, the package is not a full structural reset of the US-China relationship.

For global China+1 policy, the agreements moderate but do not eliminate diversification logic. Companies may slow decisions driven purely by tariff anxiety, but they are unlikely to abandon resilience, optionality and multi-location operating models. The most affected sectors are those tied to China-linked manufacturing supply chains and critical inputs.

For India GCC business, the impact is selective. India’s GCC growth is now driven by capability arbitrage, AI, digital product ownership, cybersecurity, data, finance, engineering and global decision participation. The India GCC opportunity therefore remains strong, though go-to-market narratives should mature from China+1 fear to enterprise value creation, resilience and AI-native transformation.

References Used:

|

ID |

Source | Title | Date |

Use in analysis |

| S1 | The White House | Fact Sheet: President Donald J. Trump Secures Historic Deals with China, Delivering for American Workers, Farmers, and Industry | 17 May 2026 | Official fact sheet listing Boards of Trade/Investment, critical minerals, Boeing aircraft, agriculture, beef and poultry access. |

| S2 | China State Council / Xinhua | China, U.S. agree to expand two-way trade under reciprocal tariff reduction framework: China’s top diplomat | 15 May 2026 | Official Chinese-source confirmation of reciprocal tariff-reduction framework and trade/investment councils. |

| S3 | Reuters | Explainer: What do China’s new US farm purchases mean for global trade? | 18 May 2026 | Independent analysis of agricultural purchase volumes, commodity redirection and global supplier impact. |

| S4 | The White House | Fact Sheet: President Donald J. Trump Strikes Deal on Economic and Trade Relations with China | 1 Nov 2025 | Prior truce layer including rare earths, soybean commitments, retaliatory tariffs and non-tariff countermeasures. |

| S5 | Reuters | Global centres in India slow hiring as AI reshapes work, ANSR CEO says | 18 May 2026 | Current GCC hiring and AI-shaping evidence from ANSR and Nasscom-Zinnov figures. |

| S6 | Express Computer / Nasscom-Zinnov report coverage | India’s GCCs are increasingly leading the AI mandate for global enterprises, driving global value creation | 7 May 2026 | 2026 India GCC landscape data: 2,117 GCCs, 3,728 units, 2.36 million employment, US$98.4bn revenue, AI/ML penetration. |

| S7 | EY India | EY GCC Pulse Survey 2025 press release | 23 Nov 2025 | Agentic AI, GenAI, innovation teams and global decision accountability in India GCCs. |

| S8 | Institute of Strategic & International Studies Malaysia | Driving factors of China Plus One | 2025 | Definition and drivers of China+1 as de-risking while maintaining China presence. |

| S9 | South China Morning Post | China and US agree to establish trade and investment councils after Xi-Trump summit | 16 May 2026 | Additional reporting on China MOC statement, tariff councils, agricultural trade and aircraft/engine arrangements. |